For a fourth straight month, the Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, expanded above growth neutral.

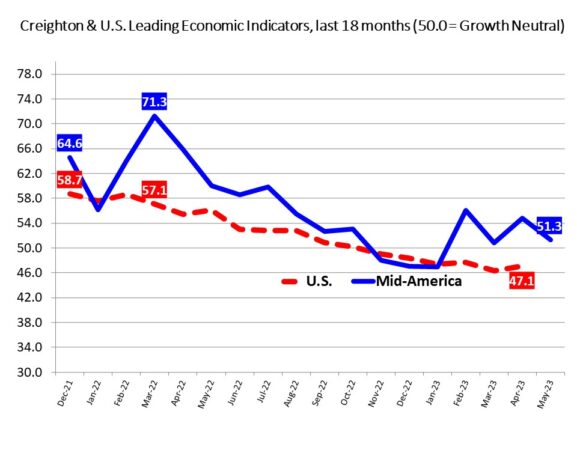

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to 51.3 from 54.8 in April.

The Mid-America report is produced independently from the national ISM.

“After flashing recession warning signals between November 2022 and January 2023, Creighton’s monthly survey of manufacturing supply managers over the past several months is now pointing to positive but slow growth with somewhat lower inflationary pressures at the wholesale level,” said Ernie Goss, PhD, director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business.

“While it’s too early to tell if the Federal Reserve is achieving its ‘soft landing,’ results from Creighton’s surveys over the last several months are somewhat promising on the growth and inflation fronts. As a result, I expect the Federal Reserve’s interest rate setting committee, the FOMC, to leave short-term interest rates unchanged at its June 13-14 meetings,” said Goss.

Other comments from supply managers in May:

- “I believe that a recession is here and may get worse before we see any improvement. Thus, I believe that inflation will continue and possibly grow.”

- “Anticipated average increase of 5-6% (inflation).”

- “Demand is down. Inflation is still too high. Stagflation.”

- “All signs we are headed in the wrong direction, and we will pay a price for our ignorance.”

- “Inflation is an illegal tax.”

“Employment growth and levels remain solid due to manufacturers’ labor hoarding. That is, manufacturers in the region are maintaining employment levels due to a fear of an inability to hire back once business activity levels pick up,” said Goss.

Confidence: Looking ahead six months, economic optimism as captured by the May Business Confidence Index slumped to a very weak 29.6 from 31.9 in April. “Approximately 40.9% of supply managers expect economic growth to decline in the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, rose to 59.1 from April’s 54.3. “Manufacturing firms have begun returning inventory to normal levels. This will support moderate sales growth in the months ahead,” said Goss.

Trade: Trade numbers were once again weak for the month with new export orders rising to a weak 46.2 from April’s 42.9. On the other hand, imports climbed to 52.8 from 47.0 in April.

Other survey components of the May Business Conditions Index were: new orders fell to 52.4 from 58.7 in April; the production or sales index sank to 52.1 from 60.9 in April; and the speed of deliveries of raw materials and supplies slumped to 41.0 from April’s 47.9. The decrease indicates a fall in supply chain disruptions and delivery bottlenecks for the month.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Arkansas: The state’s May Business Conditions Index sank to 50.4 from 52.4 in April. Components from the May survey of supply managers were: new orders at 52.2; production or sales at 50.7; delivery lead time at 41.0; inventories at 57.5; and employment at 50.9. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 1.7% over the past 12 months while manufacturing hourly wages climbed by 5.0% over the same time period.

Iowa: The state’s Business Conditions Index for May fell to 51.9 from April’s 55.8. Components of the overall May index were: new orders at 52.3; production or sales at 51.1; delivery lead time at 41.4; employment at 54.4; and inventories at 60.4. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 1.9% over the past 12 months while manufacturing hourly wages climbed by 6.9% over the same time period.

Kansas: The Kansas Business Conditions Index for May dropped to 43.1 from April’s 49.7. Components of the leading economic indicator from the monthly survey of supply managers for May were: new orders at 51.0; production or sales at 47.3; delivery lead time at 37.2; employment at 48.9; and inventories at 31.1. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 3.0% over the past 12 months while manufacturing hourly wages climbed by 10.6% over the same time period.

Minnesota: The May Business Conditions Index for Minnesota sank to 51.1 from 54.2 in April. Components of the overall May index were: new orders at 52.2; production or sales at 50.9; delivery lead time at 41.2; inventories at 58.8; and employment at 52.4. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 1.3% over the past 12 months while manufacturing hourly wages climbed by 2.4% over the same time period.

Missouri: The state’s May Business Conditions Index rose to 51.2 from 49.5 in April. Components of the overall index from the survey of supply managers for May were: new orders at 53.0; production or sales at 51.2; delivery lead time at 41.1; inventories at 58.5; and employment at 52.2. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 4.3% over the past 12 months while manufacturing hourly wages climbed by 6.8% over the same time period.

Nebraska: For a fifth straight month, Nebraska’s Business Conditions Index climbed above the growth neutral threshold. The overall reading for May declined to 51.0 from 56.8 in April. Components of the index from the monthly survey of supply managers for May were: new orders at 52.2; production or sales at 50.9; delivery lead time at 41.1; inventories at 58.6; and employment at 52.2. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 3.0% over the past 12 months while manufacturing hourly wages climbed by 4.6% over the same time period.

North Dakota: The state’s Business Conditions Index climbed above growth neutral for May with a reading of 56.0, but was down from 56.9 in April. Components of the overall index for May were: new orders at 52.6; production or sales at 52.2; delivery lead time at 42.6; employment at 64.1; and inventories at 68.5. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 1.7% over the past 12 months while manufacturing hourly wages climbed by 3.6% over the same time period.

Oklahoma: Oklahoma’s Business Conditions Index dipped in May to a reading below growth neutral. The May index slumped to 44.7 from 54.5 in April. Components of the overall May index were: new orders at 51.7; production or sales at 49.2; delivery lead time at 39.3; inventories at 46.0; and employment at 37.1. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 2.9% over the past 12 months while manufacturing hourly wages climbed by 5.0% over the same time period.

South Dakota: The May Business Conditions Index for South Dakota climbed to a solid 56.9 from April’s 56.7. Components of the overall index from the May survey of supply managers in the state were: new orders at 52.7; production or sales at 52.4; delivery lead time at 42.8; inventories at 70.4; and employment at 66.3. According to U.S. Bureau of Labor Statistics data, manufacturing employment in the state expanded by 2.5% over the past 12 months while manufacturing hourly wages climbed by 9.9% over the same time period.

Survey results for June will be released on July 3, 2023, the first business day of the month.